Introduction: Bharat Coking Coal Limited (BCCL) is a wholly-owned subsidiary of Coal India Limited, India’s largest coal producer. Incorporated in 1972 and granted Mini Ratna status in 2014, BCCL was established with a focused mandate to mine and supply coking coal—a critical raw material for steelmaking, where domestic availability in India is structurally constrained. In Fiscal 2025, BCCL accounted for 58.5% of India’s total coking coal production, highlighting its strategic importance to the domestic steel ecosystem.

What Does the Company Do? BCCL holds one of the largest coking coal reserves in India, with estimated reserves of approximately 7,910 million tonnes as of April 1, 2024. Its mining operations are concentrated in two of India’s most important coal belts:

Jharia Coalfield in Jharkhand (252.88 sq. km)

Raniganj Coalfield in West Bengal (35.43 sq. km).

The company operates over a total leasehold area of 288.31 sq. km, providing long-term resource visibility. As of September 30, 2025, BCCL operated 34 mines, including:

26 opencast mines

4 underground mines

4 mixed mines.

*Opencast mining forms the backbone of its operations, contributing over 97% of total coal production, reflecting higher productivity and cost efficiency compared to underground mining.

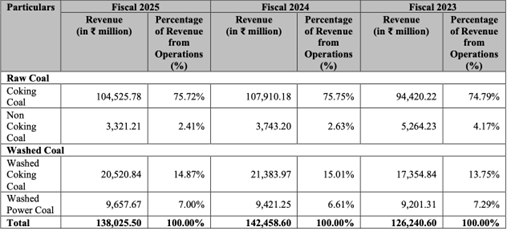

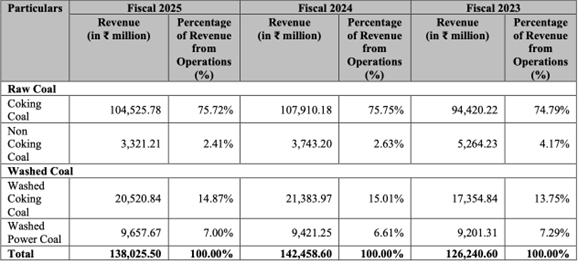

Revenue from lines of Business:

Majority of BCCL’s revenue comes from Coking Coal at 75.72% for fiscal 2025 and it has been a stable source of revenue since the Fiscal 2023.

The other major source of revenue after Coking coal is Washed Coal stands at 14.87% of its total revenue for fiscal 2025.

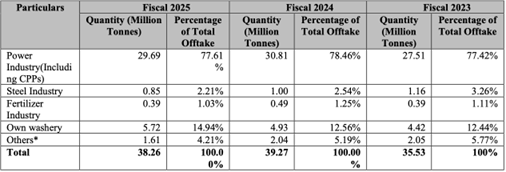

Majority of the BCCL’s consumer is coming from Power Industry as it consumes 77.61% of BCCL’s coal supply for fiscal 2025 and the other major consumer is Steel Industry at 2.21%.

Industry Context: Coking Coal Demand vs Supply:

In Fiscal 2025, India’s coking coal demand stood at 67 million metric tonnes (MMT) and is projected to increase to 138 MMT by Fiscal 2035. While total coking coal supply appears surplus in several years, this surplus is largely optical. The reason is that only a limited portion of domestically produced coking coal can be directly used in steelmaking due to its inferior quality. Going forward, even if aggregate supply remains higher than demand, the demand for coking coal suitable for steel production is expected to increase.

How Indian Coking Coal Is Actually Used

Indian coking coal generally has high ash content (18–35%) and produces low-strength coke if used independently. As a result, very little domestic coking coal is used “as-is” in steelmaking.

The primary use of Indian coking coal is blending with imported high-quality coking coal. Steel plants typically import prime coking coal from countries such as Australia, the US, and Canada, and blend it with washed Indian coking coal to produce coke with acceptable strength and ash levels. A typical blend consists of 60–70% imported coking coal and 30–40% washed Indian coking coal. Without domestic coal, import dependence would rise to nearly 100%, significantly increasing steel production costs. This makes PSUs like BCCL strategically important despite the quality limitations of Indian coking coal.

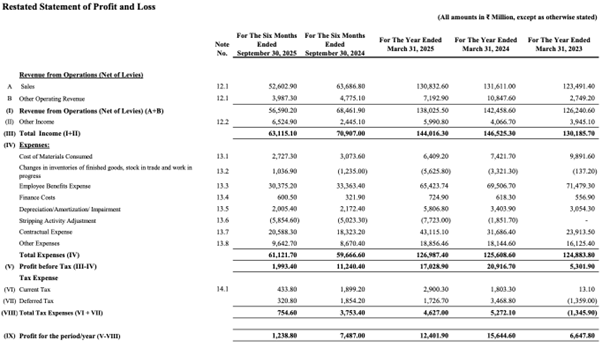

Financial Performance

Over the period from Fiscal 2023 to Fiscal 2025, BCCL reported the following compound annual growth rates (CAGR):

Revenue CAGR: 5.2%

EBITDA CAGR: 62.6%

PAT CAGR: 36.6%

These figures indicate improving profitability metrics during the period under review.

Key Risks

A significant portion of BCCL’s revenues is derived from raw coking coal, which contributed between approximately 75.72% and 75.75% of revenue from operations across recent fiscal periods. Any decline in demand for raw coking coal could adversely affect the company’s business, financial condition, and cash flows.

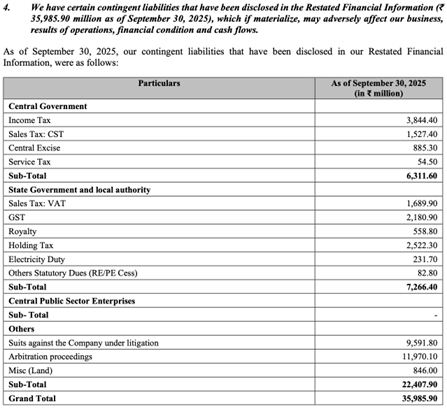

The company also has contingent liabilities that are approximately 2x its Profit Before Tax (PBT) and 3x its Profit After Tax (PAT).

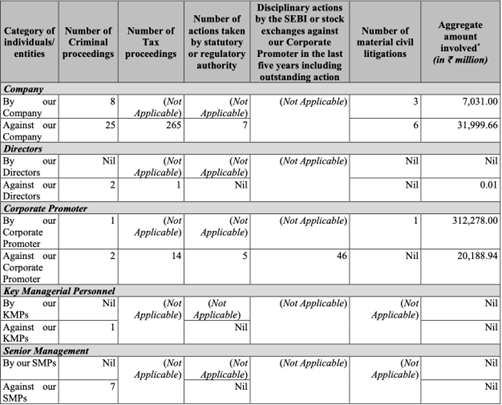

Additionally, pending litigations amount to around 22.2% of total income, calculated as ₹31,999.66 crore against total income of ₹144,016.30 crore.

Peer Comparison & Valuation

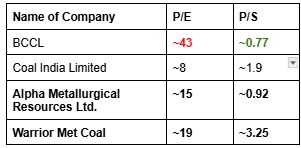

Post-IPO, BCCL is expected to trade at a P/E multiple of approximately 43.23, with a PEG ratio of around 1.19. In comparison, Coal India Limited trades at a significantly lower P/E of around 8.43. From a price-to-sales perspective, BCCL’s P/S multiple is approximately 0.77, compared with Coal India’s ~1.9. International peers trade at P/S multiples ranging from approximately 0.92 to 3.25 and P/E multiples in the range of 15 to 19.

This indicates that while BCCL appears relatively expensive on an earnings basis, it looks comparatively reasonable when viewed through the lens of revenue multiples.